Research from Savills World Research team suggests that residential and industrial property will be the strongest real estate asset classes globally in 2022, and that total investment volumes bounced back very strongly in 2021 as an increasing number of funds looked to invest into real estate.

In an update to Impacts, its global research programme, Savills says that in the 12 months to November 2021 global real estate investment volumes rose 38% on the same period in 2020 to US$1.3 trillion. The number of funds targeting real estate also reached new heights as investors sought to diversify income streams: 1,250 real estate funds targeting $365 billion in capital between them were identified in 2021, according to Preqin data, up from the approximately 1,000 funds that were active in 2020.

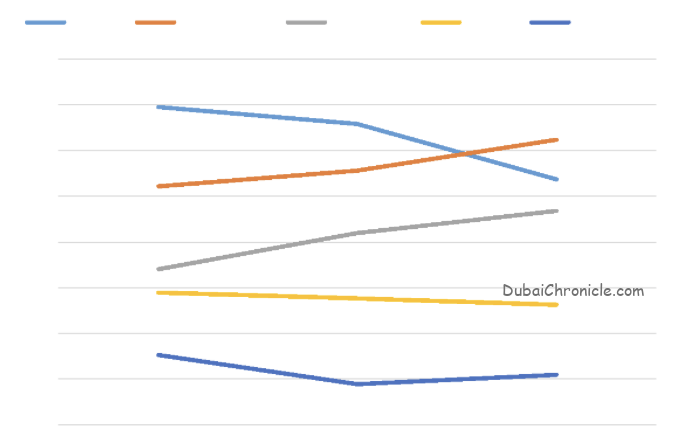

According to Savills, while global investment in the offices sector remains below pre-pandemic levels, volumes in the highly sought-after industrial sector rose 54%; this is likely to continue throughout 2022. Residential (namely multifamily, but also student and senior housing) became the largest sector for investment globally in 2021, overtaking offices for the first time (see chart). The international real estate advisor says that investors are increasingly attracted to residential’s secure, income generating qualities, robust underlying demand, and resilience against technological disintermediation, but while strong activity will continue in 2022 a dearth of standing stock means that development will be the entry point for many.

Share of total global real estate investment, by year:

Source: Savills Research using RCA, data covers 12 months to November of stated year

Closer to home, the following investment themes emerged for the Middle East.

Swapnil Pillai, Associate Director, Middle East Research said: “Covid-19 accelerated trends that were already set in motion before the pandemic took hold. While industrial has emerged as a strong but natural winner as a result of a flourishing e-commerce sector, prime offices found favour once again across the Middle East markets as employees returned to the workplace. As population growth picks up again, especially in the UAE and Saudi Arabia, residential development will continue to remain a key focus area.

Paul Tostevin, Director in the World Research team, adds: “While the stats show offices were less loved than residential last year, despite the multitude of headlines about ecommerce growth they still made up a greater proportion of the global market than industrial. With cross border investors, particularly in Europe, focusing on ESG strategies in 2022 we’re likely to see opportunities to redevelop, reconfigure and repurpose office stock into high-performing sustainable assets, while in much of Asia and the Middle East the office is still very much the backbone of working life. Retail bricks and mortar, while maligned in some markets, is still at the heart of the consumer experience in China, for example, even with its extremely high online penetration rate, while in the West, pricing of some assets now looks competitive and 2022 may see more opportunistic investment in the sector.”

{kind=link}