Since the global synchronized growth of 2017, economic conditions have been gradually weakening and will produce an across-the-board deceleration in the months ahead. Beyond that, the prospect for markets and national economies will depend on a broad range of factors, some of which do not bode well.

After the synchronized global economic expansion of 2017 came the asynchronous growth of 2018, when most countries other than the United States started to experience slowdowns. Worries about US inflation, the US Federal Reserve’s policy trajectory, ongoing trade wars, Italian budget and debt woes, China’s slowdown, and emerging markets fragility led to a sharp fall in global equity markets toward the end of the year.

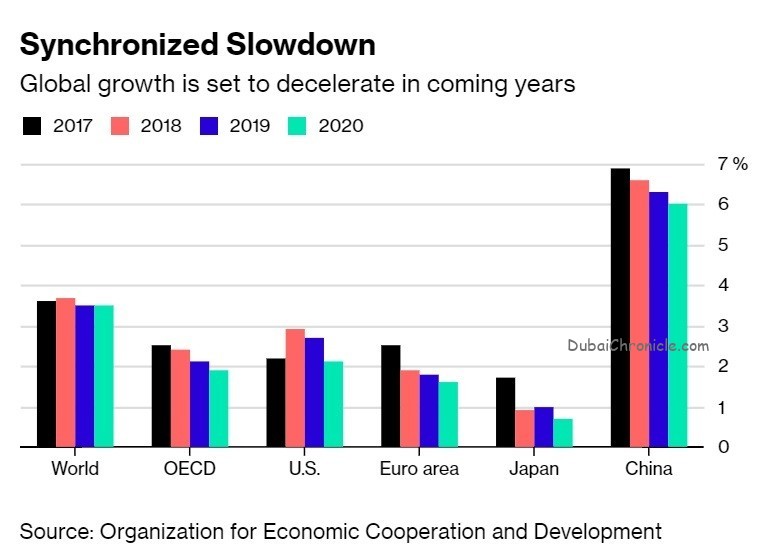

The good news at the start of 2019 is that the risk of an outright global recession is low. The bad news is that we are heading into a year of synchronized global deceleration; growth will fall toward – and, in some cases, below – potential in most regions.

Since the global synchronized growth of 2017, economic conditions have been gradually weakening and will produce an across-the-board deceleration in the months ahead. Beyond that, the prospect for markets and national economies will depend on a broad range of factors, some of which do not bode well.

After the synchronized global economic expansion of 2017 came the asynchronous growth of 2018, when most countries other than the United States started to experience slowdowns. Worries about US inflation, the US Federal Reserve’s policy trajectory, ongoing trade wars, Italian budget and debt woes, China’s slowdown, and emerging-market fragilities led to a sharp fall in global equity markets toward the end of the year.

The good news at the start of 2019 is that the risk of an outright global recession is low. The bad news is that we are heading into a year of synchronized global deceleration; growth will fall toward – and, in some cases, below – potential in most regions.

Sixth, equity markets in the US and elsewhere are still overvalued, even after the recent correction. As wage costs rise, weaker US earnings and profit margins in the coming months could be an unwelcome surprise. With highly indebted firms facing the possibility of rising short- and long-term borrowing costs, and with many tech stocks in need of further corrections, the danger of another risk-off episode and market correction can’t be ruled out.

Seventh, oil prices may be driven down by a coming supply glut, owing to shale production in the US, a potential regime change in Venezuela (leading to expectations of greater production over time), and failures by OPEC countries to cooperate with one another to constrain output. While low oil prices are good for consumers, they tend to weaken US stocks and markets in oil-exporting economies, raising concerns about corporate defaults in the energy and related sectors (as happened in early 2016).

Finally, the outlook for many emerging-market economies will depend on the aforementioned global uncertainties. The chief risks include slowdowns in the US or China, higher US inflation and a subsequent tightening by the Fed, trade wars, a stronger dollar, and falling oil and commodity prices.

Though there is a cloud over the global economy, the silver lining is that it has made the major central banks more dovish, starting with the Fed and the People’s Bank of China, and quickly followed by the European Central Bank, the Bank of England, the Bank of Japan, and others. Still, the fact that most central banks are in a highly accommodative position means that there is little room for additional monetary easing. And even if fiscal policy wasn’t constrained in most regions of the world, stimulus tends to come only after a growth stall is already underway, and usually with a significant lag.

There may be enough positive factors to make this a relatively decent, if mediocre, year for the global economy. But if some of the negative scenarios outlined above materialize, the synchronized slowdown of 2019 could lead to a global growth stall and sharp market downturn in 2020.

{kind=link}