The global office investment sector, similar to other types of real estate, is coming under some pressure from the macro-economic environment. However, strong fundamentals should keep investment yields largely stable in many key markets, including Paris, London, Sydney, Mumbai and Dubai, Savills says in its first Global Capital Markets Quarterly update.

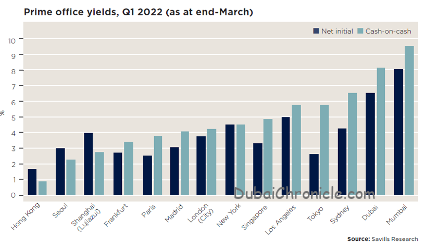

Edward Price, Associate Director – Capital Markets Middle East at Savills said: “Leasing activity across the office market in Dubai has remained strong over the last six months. The number of enquiries have gradually increased and the city has benefitted from the availability of Grade A space at affordable cost compared to other office hubs across EMEA. The office market in Dubai remains an attractive investment opportunity with estimated cash-on-cash prime office yields over 8%, second only to Mumbai and highest among the western and Asian countries ranked.”

Savills has assessed the likely interplay between the top-down (inflation, interest rate rises, geopolitical uncertainty) and bottom-up factors (limited availability of stock and weight of money causing competition between investors) that will determine the pricing of office assets over the next 12 months in major global cities.

The US may be most exposed to macro top-down factors, with expectations of a significant tightening in financial conditions and limited pricing power for landlords potentially leading to yields rising in New York and Los Angeles. European investors meanwhile may continue to benefit from solid occupier demand and a lack of supply in the prime and core segments of the market, keeping yields stable.

Meanwhile, in Asia, domestic market-specific characteristics dominate the regional narrative. In Tokyo for example, cash-on-cash returns will remain attractive given little upward pressure on interest rates, which will support further yield compression, while the outlook for Shanghai has deteriorated amid a challenging domestic economic backdrop.

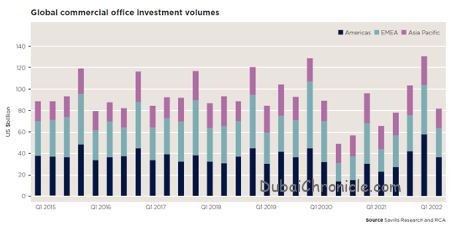

The recovery in occupier demand and a shortage of prime office stock across most major markets has encouraged greater investor activity. Global investment in offices hit a record of US$130 billion in the final quarter of 2021, with momentum spilling into the beginning of this year. The US$82 billion transacted globally in Q1 was up 25% on the year, and only 3.5% shy of the five-year average leading up to Covid-19.

Increased uncertainty will underpin a flight to safety which, combined with an increasing focus on ESG, will favour Grade A office buildings in major cities.

{kind=link}